Ek Daughter, Do Schemes, Ek Confusion

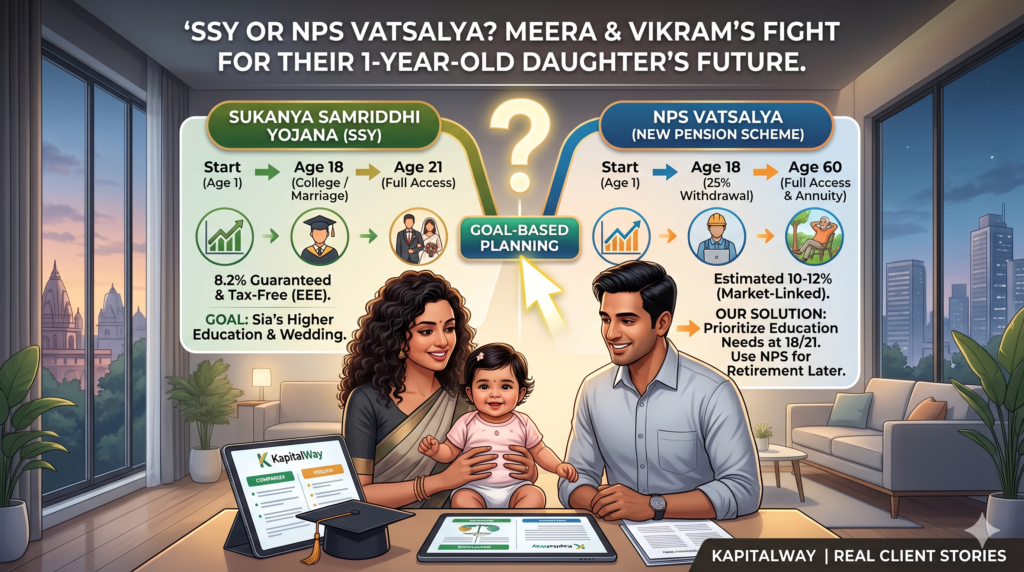

Ek Daughter, Do Schemes, Ek Confusion — KapitalWay Her Daughter Was Just 1 Year Old — But Her Parents Had Been Fighting Over This Investment Decision for 3 Months A real story from our client files — the question every new parent in India is asking, and exactly how we helped them settle it 👤 CLIENT Meera & Vikram T. Name Changed Meera — Talent Acquisition Expert Vikram — IT Professional Kanpur Meera and Vikram had been married for three years. Their daughter Sia had just turned one. Between them, they bring home a combined income of ₹78,000 a month. They had a PPF account, a small LIC endowment policy, and a recurring deposit running at the post office. Financially, they were cautious, careful people — the kind who read before they sign. When Sia was born, they promised themselves they would start something specifically for her — something that would still be standing when she needed it most. But they couldn’t agree on what. ⚠️ THE SITUATION Meera had heard about Sukanya Samriddhi Yojana from a colleague at work. The returns sounded solid — government-backed, safe, fixed interest, and the account was specifically for girl children. It felt personal. It felt right. Vikram had a different view. He had read about NPS Vatsalya after it launched in late 2024. “10 to 12% returns, no upper limit on investment, market-linked growth” — to him, SSY at 8.2% sounded like they were leaving money on the table. For three months, they went back and forth. Neither was wrong — but neither had the complete picture. When they finally came to us, Meera opened the conversation. “Hum dono ki baat hi nahi ban rahi. Woh kehte hain NPS Vatsalya better hai. Main kehti hun SSY safe hai. Sia ke liye kya sahi hai — yeh sirf aap hi bata sakte hain.” — Meera’s first words to us at our initial meeting 💡 OUR SOLUTION 1 Goal pehle, scheme baad mein — what does Sia actually need this money for? Before we touched any numbers, we asked one question: When do you need this money, and for what? Their answer was immediate — Sia’s college education, and if needed, her wedding. Not her retirement at 60. That single answer changed the entire conversation. NPS Vatsalya is a pension scheme. The bulk of the corpus it builds stays locked until the child is 60 years old. For parents saving for a daughter’s college at age 18 or 21, that is the wrong tool for the job — no matter how good the headline return looks. 2 Show them the withdrawal reality — not just the corpus number This is where Vikram’s assumption broke down. We put both schemes on paper with the same investment — ₹60,000 per year — starting from when Sia is 1 year old. Sukanya Samriddhi (SSY) NPS Vatsalya Estimated corpus at age 18 ~₹25.8 lakh ~₹30.4 lakh Withdrawal allowed at 18 50% for education 25% for education/illness Usable money at age 18 ~₹12.9 lakh ✅ ~₹7.6 lakh Full access At age 21 At age 60 Tax on maturity Zero — fully EEE ✅ 40% annuity is taxable NPS Vatsalya builds a bigger total number. But SSY puts more actual rupees in Sia’s hands at 18 when she needs them for college — and the full amount by 21. Vikram stared at the table for a long time. “Yeh toh maine kabhi socha hi nahi tha,” he said quietly. 3 Resolve the tax confusion — the ₹50,000 deduction doesn’t need Sia’s account Vikram’s other reason for NPS Vatsalya was the extra ₹50,000 deduction under Section 80CCD(1B). What he didn’t know is that this deduction can be claimed on his own NPS account — which he already had through his IT employer. He did not need to open NPS Vatsalya for Sia to unlock that benefit. Topping up his own NPS by ₹50,000 this year was all it took. Two birds, one stone. 4 Open SSY immediately — every month of delay costs compounding SSY can only be opened for a girl child below 10 years of age. Sia was 1. Every month they delayed was one less month of compounding at 8.2% — guaranteed and fully tax-free. We helped Meera open the account at their nearest authorised bank branch the same week. The first deposit of ₹12,500 went in immediately. Going forward, they plan to deposit ₹1.5 lakh per year — the maximum — to make Sia’s corpus as full as possible. 5 Keep NPS Vatsalya as a future option — not a pressure decision today We did not tell Vikram to forget NPS Vatsalya forever. If in two or three years their income grows and they want to add a second layer of long-term wealth for Sia — one she manages herself after turning 18 — NPS Vatsalya can still be opened then. She will still be under 18. The door stays open. But today, with one goal (education) and one daughter, SSY was the clear first move. ⏳ WHERE WE STAND NOW The confusion has been resolved. Sia has her Sukanya Samriddhi account. Vikram has topped up his own NPS to claim the extra ₹50,000 deduction. The family has a clean, clear plan — and nobody is arguing anymore. ✅ Done — SSY Account Opened Sia’s account is active, first deposit made, passbook in Meera’s hand ✅ Done — Tax Plan Fixed Vikram’s own NPS topped up — ₹50,000 extra deduction claimed without locking Sia’s money till 60 ✅ Done — Annual Investment Plan Set ₹1.5 lakh/year into SSY locked in; NPS Vatsalya revisit planned when income grows ⏳ In Progress — Sia’s Corpus Growing 20 years of compounding ahead — we will be watching every step “Pehle lagta tha ki yeh decision bahut complicated hai. Lekin jab humne samjha ki Sia ke liye paise kab chahiye aur kitne chahiye — sab clear ho gaya. Ab main aur Vikram dono ek page par hain. Aur Sia ka future

Ek Daughter, Do Schemes, Ek Confusion Read More »